May 6'th 2010 Flash Crash Analysis

Continuing Developments

Delays on 04-28-2010

The Effects of "High Frequency

Quoting"

Publication Date: September 2, 2010

Back to Table

Of Contents

|

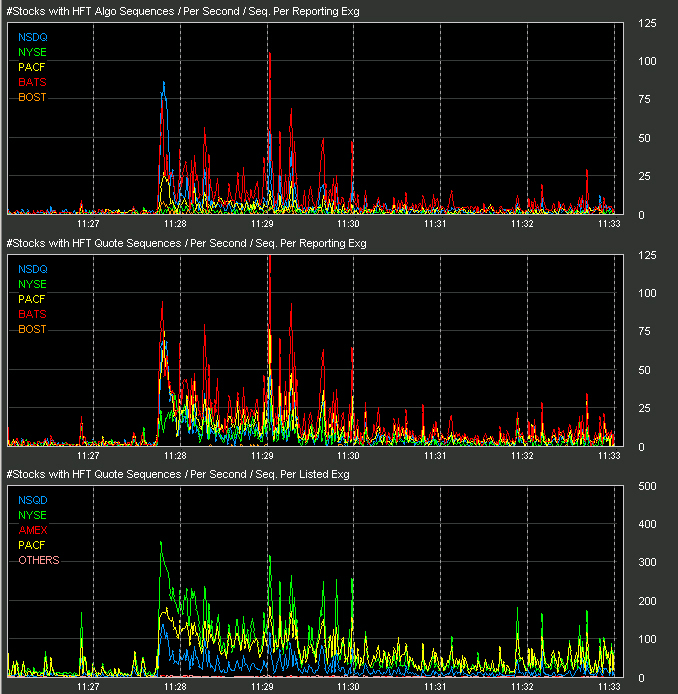

While scanning through historical data looking for previous days which exhibit

similar behaviour to that of

05/06/2010,

we noticed the following spike in our HFT monitors on 04/28/2010 at

11:27:46:

We decided to investigate this further to determine if any stocks experienced

the same delays from the high quote activity that started at 11:27:42 which we

saw on 05/06/2010 and reported on in our initial

Flash

Crash Analysis. We found many.

Note that this was just one week prior to 05/06/2010, the day of the flash

crash. The warning signs were present. |

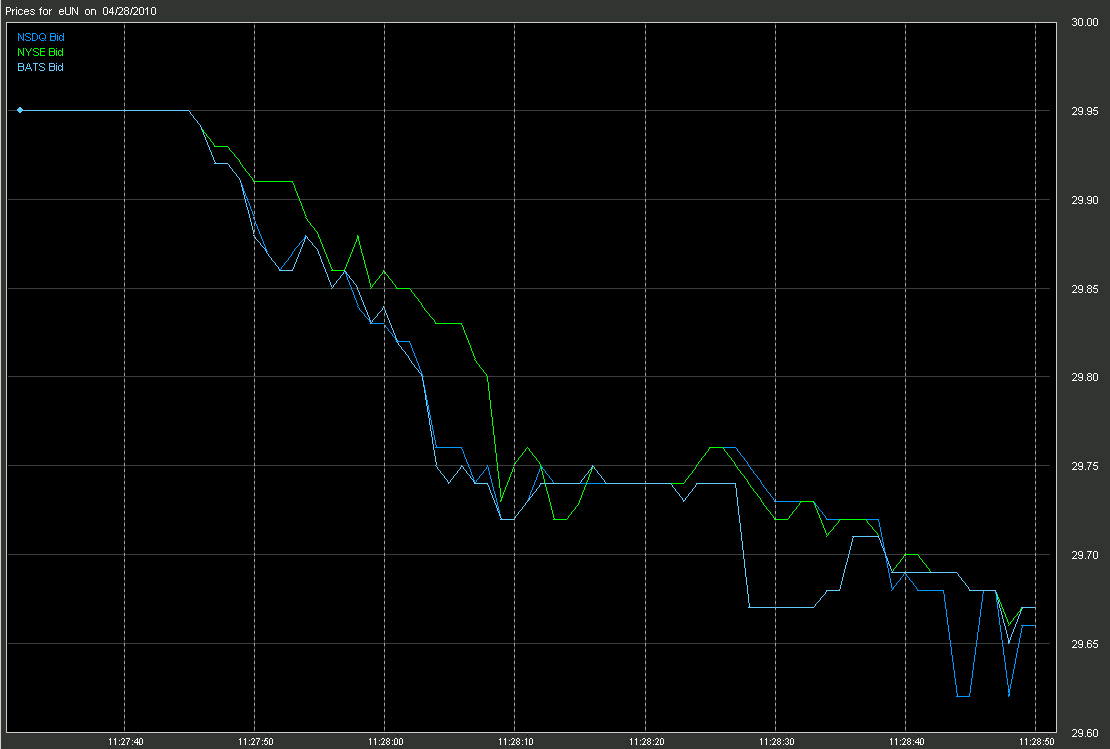

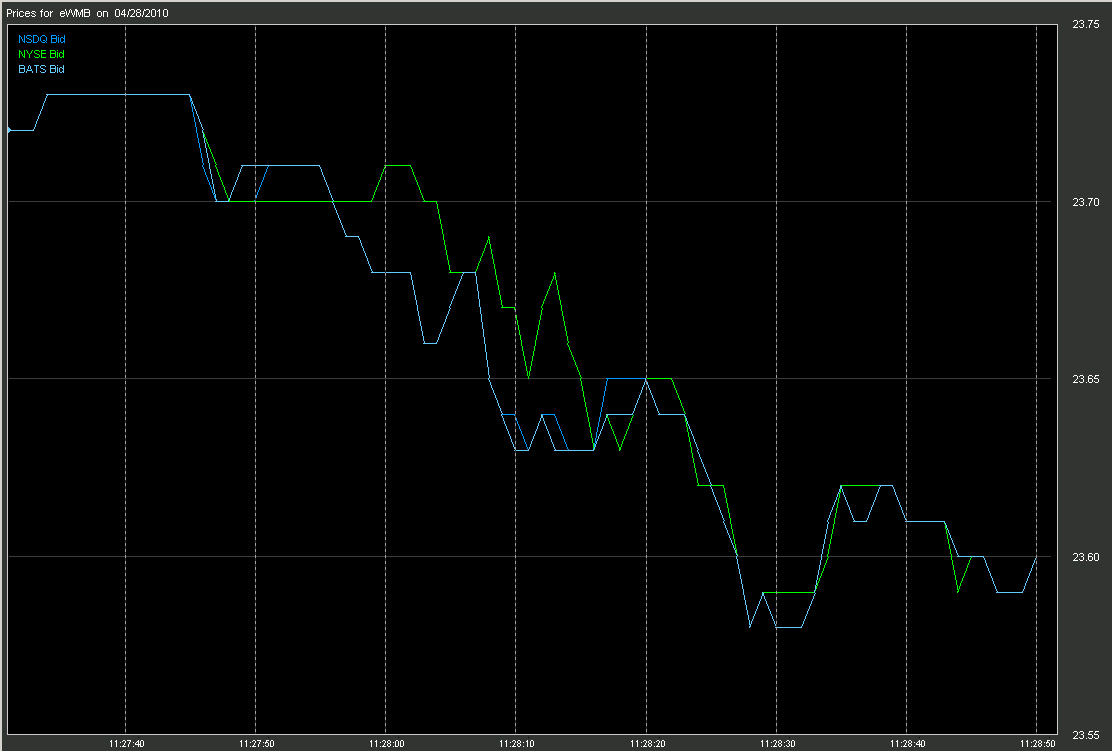

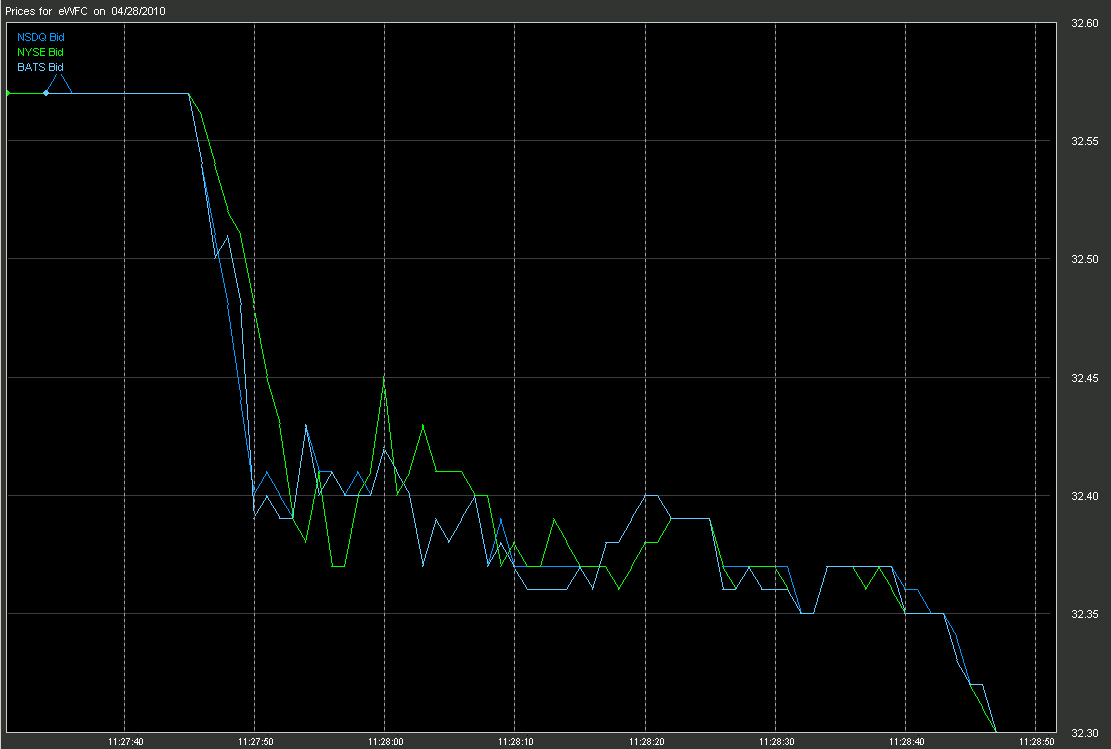

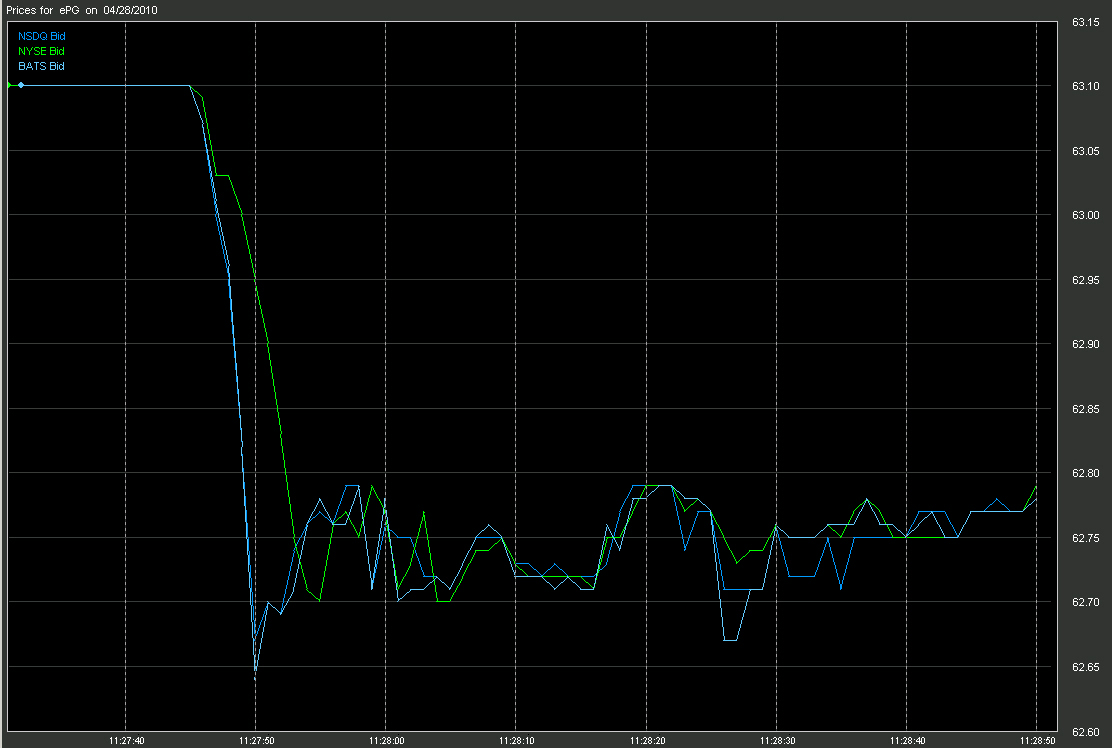

Delays

Seconds after the high quote rates began NYSE quotes began to lag the market.

Here we show four stocks that were found to have delays in the NYSE quotes on

4/28/2010. These four were chosen at random and there are many other not shown

that also experienced the delay.

As we pointed out in our "Latency On

Demand" report, if the average or base quote rate is around

10,000/second, then it only takes an additional 10,000 quotes/second to reach

the magic 20,000 quotes/seconds where a corresponding delay is seen in NYSE

quote from CQS. This 10,000 quotes/second can be in any stock or combination of

stocks that NYSE sends quotes to CQS for.

(click on the smaller charts for a full size image)

|

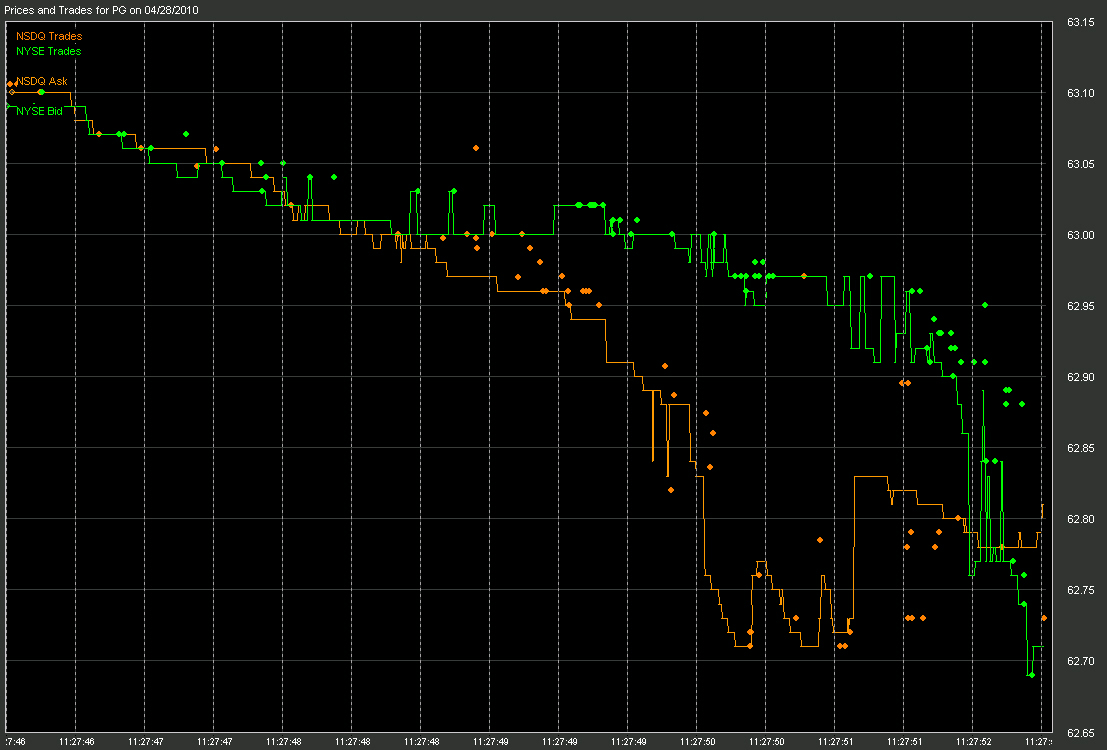

What we demonstrate in this report is this; when the NBBO ask dropped below

the NYSE bid, trade executions are seen from NYSE that equal the NYSE bid and

trade executions from other exchanges at the NBBO ask. This clearly

demonstrates that CQS does indeed influence and drive trading.

For our detailed trade analysis, we decided to focus on PG (Proctor &

Gamble). Note in the chart below the NYSE quotes began to lag the market at

11:27:45 and continued to lag through 11:28:00. |

In the following charts, trades are plotted as a circle,

bid and ask prices as a line.

Here we see trades occuring on the NYSE exchange at the NYSE bid price and on

NASDAQ at the NASDAQ ask price. This is very significant. It shows that

the cross in CQS drives trading.

|

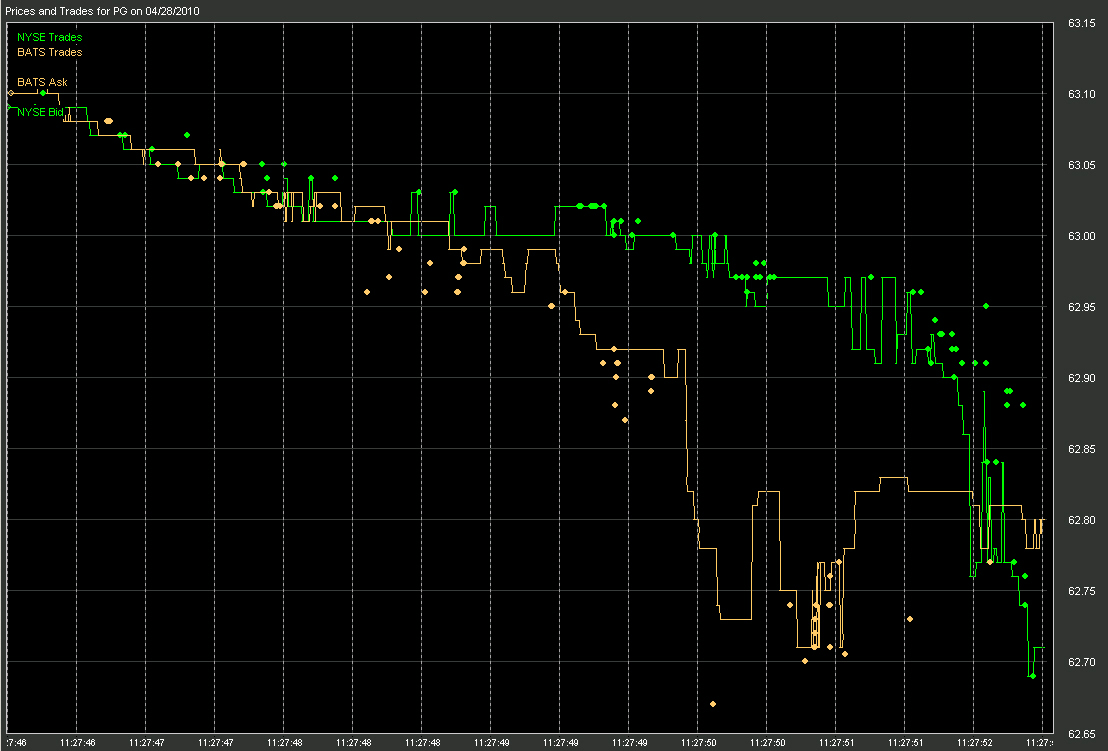

Here again we see trades occuring on the NYSE exchange at the NYSE bid

price and on BATS at the BATS ask price.

|

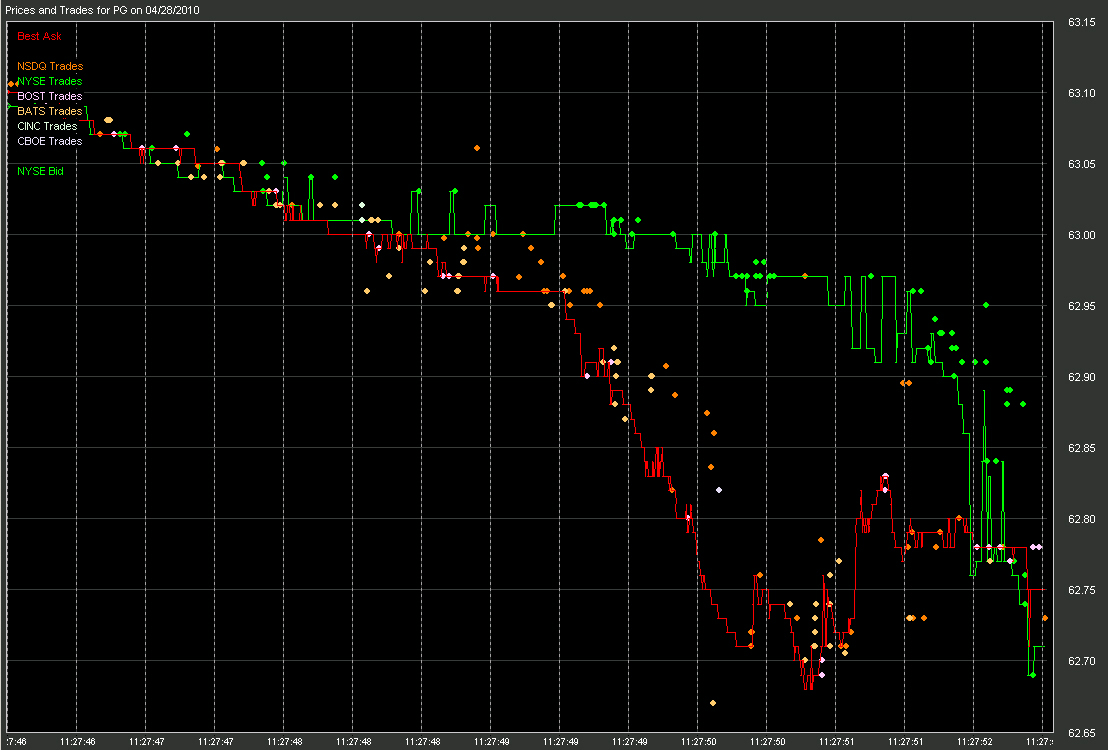

Finally we show the NBBO ask price, the NYSE bid price and trades from

various reporting exchanges. It is easy to determine here that the NYSE price

is lagging and severely crossed with the NBBO ask. As in the previous charts,

trades occured on the NYSE exchange at the NYSE bid price and on other

exchanges near the NBBO ask price.

|

| |

Inquiries: pr@nanex.net

Publication Date: September 2, 2010

http://www.nanex.net

| This report and all material shown on this

website is published by Nanex, LLC and may not be reproduced, disseminated, or

distributed, in part or in whole, by any means, outside of the recipient's

organization without express written authorization from Nanex. It is a

violation of federal copyright law to reproduce all or part of this publication

or its contents by any means. This material does not constitute a solicitation

for the purchase or sale of any securities or investments. The opinions

expressed herein are based on publicly available information and are considered

reliable. However, Nanex makes NO WARRANTIES OR REPRESENTATIONS OF ANY SORT

with respect to this report. Any person using this material does so solely at

their own risk and Nanex and/or its employees shall be under no liability

whatsoever in any respect thereof. |

|

|

|