One item we have uncovered is an exception of Rule 611 contained in

Reg NMS. We believe this may hold another key in how the rapid firing

of quotes can give an advantage.

To understand how one could exploit this exception, consider how the exchanges

track their own internal NBBO:

The exchanges don't use CQS for routing. This means they receive their

information from direct links to other exchanges to compute the NBBO internally

and route based on that. In other words, each exchange is recreating what CQS

does. Due to the flickering quote exception, an exchange can ignore quotes from

another exchange that are changing more than once per second.

Because an exchange can ignore flickering quotes, you have no idea how the

quotes are factored into the exchanges internal NBBO and therefore, no idea

where the order will be routed to.

CQS does not take the flickering quote exception into consideration -- CQS

allows the quotes to set the NBBO.

If an entity broadcasts quotes rapidly that flicker the price and it is known

these quotes will be ignored by an exchange but be broadcast to the public over

CQS (and shown as the current NBBO), the entity may then have an

advantage.

To better understand this, we have created an application that reads historical

data and produces a movie of how exchange routing works. The video below shows

routing of GE orders on 05/06/2010:

Is this strategy being employed? We don't know. What we know is that it

could be and in fact the concern was raised in Reg NMS:

Page 102:One commenter opposed the exception because it believed that

it would create an arbitrage opportunity that could be taken advantage of by

computerized market participants. Another commenter expressed concern that

the exception would enable trading centers to execute trades internally and

route orders using the worst quotation during the one second window.

We leave it to the regulatory agencies to determine if indeed market

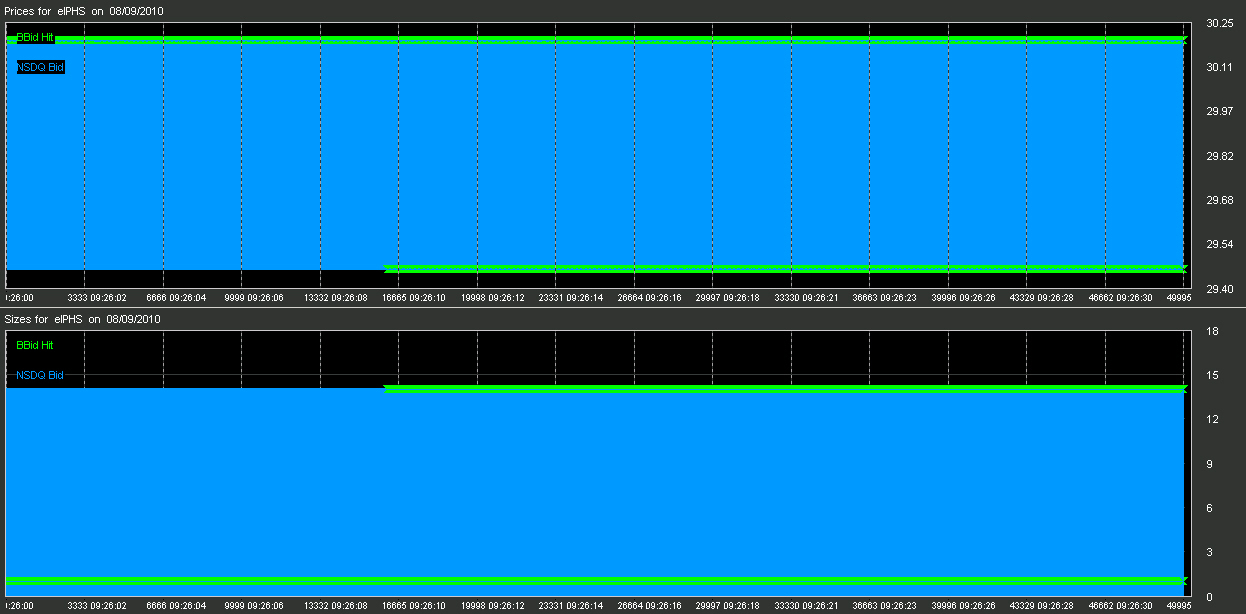

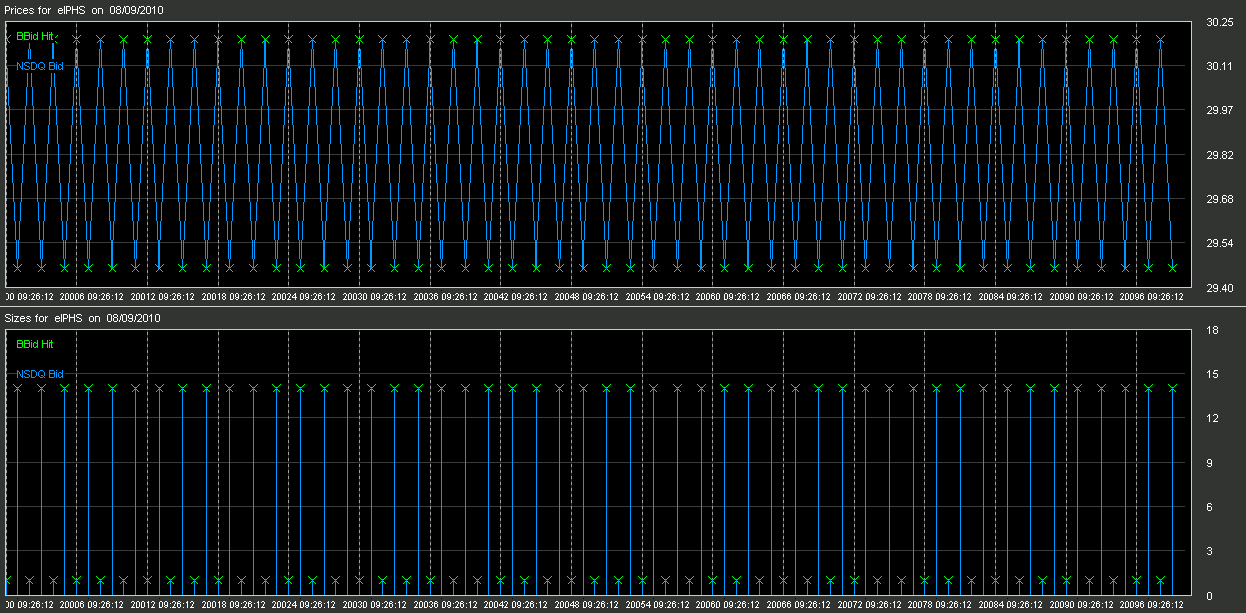

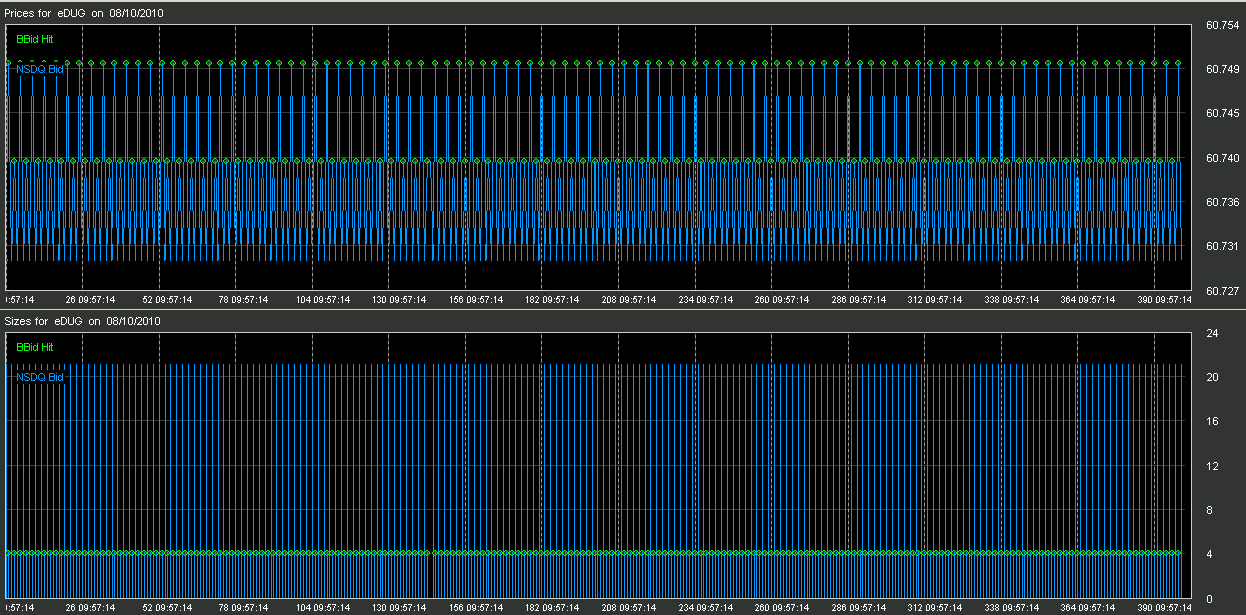

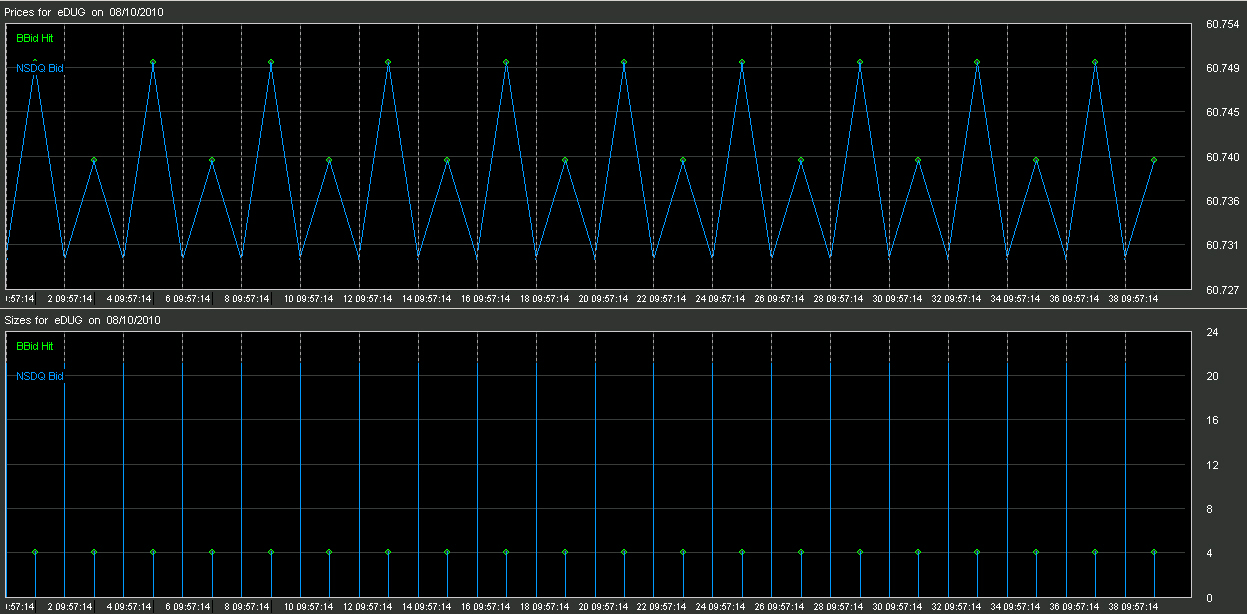

participants are taking advantage of this exception. It certainly would explain

a few of the rapid fire price/cycling high rate quote burst we see on a daily

basis and present on our "Crop Circle of the

Day" page.

This report and all material shown on this

website is published by Nanex, LLC and may not be reproduced, disseminated, or

distributed, in part or in whole, by any means, outside of the recipient's

organization without express written authorization from Nanex. It is a

violation of federal copyright law to reproduce all or part of this publication

or its contents by any means. This material does not constitute a solicitation

for the purchase or sale of any securities or investments. The opinions

expressed herein are based on publicly available information and are considered

reliable. However, Nanex makes NO WARRANTIES OR REPRESENTATIONS OF ANY SORT

with respect to this report. Any person using this material does so solely at

their own risk and Nanex and/or its employees shall be under no liability

whatsoever in any respect thereof.