Nanex Research

Nanex ~ 06-Jan-2014 ~ First Gold Halt of 2014

On January 6, 2014 at 10:14:13, Gold futures plummeted $30 on heavy volume. About 4,200 contracts send gold futures prices tumbling $30 and trigger a 10 second trading halt.

Update: 18-Jun-2015

On June 18, 2015, the CME announced it had fined a firm because trading platform went haywire causing a mass entry of order messages which resulted in "a disruptive and rapid price movement" and prompted a Velocity Logic event. Basically, gold futures were quote stuffed to death.

We documented this event was almost a year and half ago (see charts below).

The chart below shows the entire $30 drop in the price of Gold futures that occurred

in just under 100 milliseconds (1/10th of a second). When we separated groups of trades

by a jump in the exchange sequence number (a technique to determine the size of a larger order)

we discovered there were 9 groups where the sum of the trade sizes was exactly 338 contracts! Each group is composed of widely different numbers of trades: the first

group of 338 contracts is made up of 211 trades, the second group is made up of 186

trades, and 3rd-9th: 120, 193, 97, 193, 137, 112

and 109 trades respectively.

We

show these 9 groups in the chart below.

What's more, there are other trades occurring between these groups of 338 contracts.

This was not the result of a fat finger, but rather the work of a high frequency trading algorithm that paused, and (probably) tested the market before continuing. A fat finger would not have such distinguishing features.

What is disturbing about this algorithm, is that it carefully waited so as not to trip the CME's stop logic and halt the stock. The halt was from the more lenient volatility circuit breaker after the price declined $30 in less than a second. This algo appears to have been more concerned about preventing an immediate halt, rather than getting the best prices. Since the value of the trades was close to $500 million, there aren't a lot of suspects. Add to this, the fact they didn't get "special treatment" and have the trades busted, or the price adjusted (which is what happened with the

Treasury Futures debacle just 2 short weeks before this event).

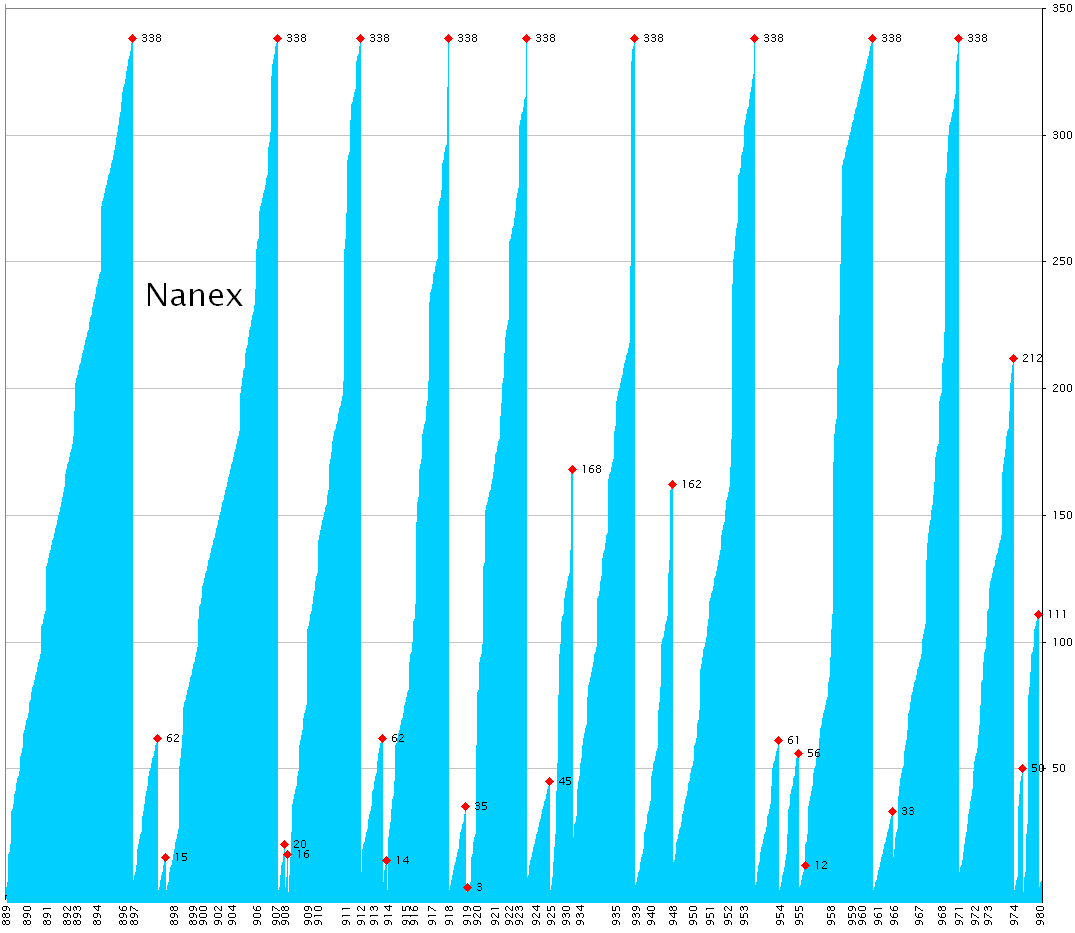

The next chart shows the cumulative sum of trade sizes for each group of trades where

a group is distinguished by a jump in the exchange sequence number. Since exchanges use one sequence number for multiple products, you can usually tell if a group of trades is the result of a larger order by the lack of gaps in the sequence number. That means no other contracts traded during that time.

The time axis is the millisecond time component of the second 10:14:12, so that the value 889 corresponds to 10:14:12.889. The value axis is the cumulative number of contracts.

The red diamond indicates the total size of a group when a sequence jump is detected.

Notice there are 9 groups that total exactly 338 contracts. Also note that each of these

groups are separated by smaller groups of trades, and 3 of these smaller groups total

61 or 62.

1. February 2014 Gold (GC) Futures

2. February 2014 Gold (GC) Futures

3. February 2014 Gold (GC) Futures

5. March 2014 Silver (SI) Futures

6. SLV ETF trades

7. GLD ETF trades

Compare the next 4 charts which all zoom in on the first 1/10th of a second of activity

(10:14:12.880 to 10:14:13) in Gold and Silver ETFs and futures. The futures trade in

Chicago, while the ETFs trade in NY. It takes information about 4 to 5 milliseconds

to travel between these two locations.

8. February 2014 Gold (GC) Futures - Zooming in on about 1/10th of a second.

9. GLD ETF trades - Zooming in on about 1/10th of a second.

Compare to Chart 8 above - note how the futures activity

starts about 5 milliseconds earlier, indicating the move started in Chicago (futures)

and not in NY (GLD).

10. March 2014 Silver (SI) Futures - Zooming in on about 1/10th of a second.

Trading didn't start in silver futures until a good 30 milliseconds after gold, which

indicates silver was reacting and not part of the same strategy affecting gold.

11. SLV ETF trades - Zooming in on about 1/10th of a second.

Activity in SLV appears 5 milliseconds after activity in GLD. The silver ETF reacts

faster to the the gold ETF (both in NY), than the silver futures reacts to gold futures

in Chicago.

12. GLD ETF trades - Zooming in on about 1/2 second of time.

Note how trades from EDGX (blue diamonds), Dark Pools (squares) and BOST (light green

circles) are reported significantly late.

13. GLD ETF - Direct Edge-X trades and NBBO

It's easier to notice the significant delay in trades reported from Direct Edge-X

Nanex Research

Inquiries: pr@nanex.net