Nanex Research

Nanex Research

Nanex ~ 01-Feb-2014 ~

What did they know,

and when did they know it?

Executive Summary

An academic paper, co-authored by the CFTC's Chief Economist at the time, Dr. Kirilenko, states that spoofing is a commonly observed form of manipulation used in High Frequency Trading (HFT) and that empirical evidence shows it exists in both equities and futures. Furthermore, spoofing relies on canceling orders fast enough so that fewer participants can trade against them. The paper uses a concrete example from actual trading data; however, because of an ongoing investigation, specifics were left out. We now know that the example was HFT spoofing crude oil futures, and the ongoing investigation led to the Panther Energy Trading fine.

This academic paper's portrayal of HFT manipulation and high quote cancel rates runs contrary to public statements made by the SEC and CFTC as well as the newly formed HFT lobbying group.

The Paper

The academic paper Behavior Based Learning In Identifying High Frequency Trading Strategies was co-authored by Dr. Andrei Kirilenko, the Chief Economist at the CFTC at the time of publication, November 7, 2011.

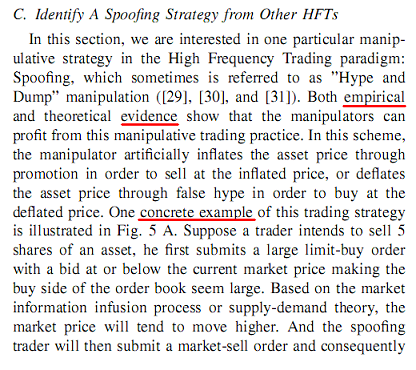

The paper establishes that there exists empirical evidence of High Frequency Trading (HFT) manipulation; specifically, a strategy known as Spoofing or "Hype and Dump":

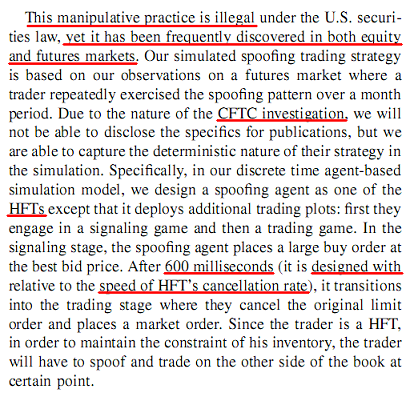

The paper affirms that spoofing is illegal and that the practice is frequently discovered in both stocks and futures:

Stock markets are regulated by the SEC, and futures by the CFTC. Since Dr. Kirilenko was a primary author of the final SEC Flash Crash Report, and because of his role as the Chief Economist for the CFTC, we know he had regular discussions with the SEC.

The paper, dated November 7, 2011, states it cannot disclose specifics due to an ongoing CFTC investigation. We firmly believe that investigation concluded with the fine against Panther Energy Trading for spoofing the oil futures markets. We analysed this case and included dozens of charts, many of which show the 600 millisecond order cancellation rate discussed in the paper.

We have since documented other events that closely resemble the Panther case, as well as thousands of other instances of questionable HFT trading practices.

Let's review the time-line:

October 1, 2010 SEC final Flash Crash Report is published. August 8, 2011 to

October 18, 2011HFT firm manipulates the oil futures markets with spoofing. November 7, 2011 An academic paper, co-authored by Dr. Kirilenko is published. The paper mentions an ongoing CFTC investigation, which turns out to be the Panther Energy fine. July 22, 2013 CFTC announces Panther Energy fine for spoofing the oil market.

It took the CFTC a full 21 months to bring action against an HFT firm for manipulating oil futures. Maybe that is the normal pace for government action, but right now, it is the least of our concern. There is something far more egregious exposed by this academic paper than the glacial pace of enforcement action, and it has to do with the question:

What did the SEC know, and when did they know it?

The paper clearly establishes that regulators (SEC and CFTC) were aware of illegal HFT manipulation strategies involving fast order cancellation rates. They knew this in November 2011, and probably many months earlier, considering the time it takes for an academic paper to get published.

If we juxtapose this knowledge with recent statements made by regulators regarding HFT, manipulation and high order cancellation rates, we see denial, uncertainty and doubt. We have even witnessed the regulator being told to shut down an academic program which was investigating other HFT manipulation strategies. That program was headed by none other than Dr. Andrei Kirilenko, who left the CFTC 2 months earlier.

What we don't see are actions or policy changes, or even discussions about reigning in HFT manipulation. This lack of regulator attention shows up in the market: the evidence of the same behavior continues to pile up, to the point that

HFT manipulators believe they are untouchable.

Just this week we refuted a claim made by a recently formed HFT lobbyist group who stated that there was no value to rapidly placing and cancelling orders and therefore HFT wouldn't do that. The week before, the CEO of an exchange expressed no concern about flickering quotes, which are a manifestation of HFT rapidly placing and cancelling orders.

Conclusion

A paper co-authored by the former CFTC Chief Economist makes it clear that regulators have known about High Frequency Trading manipulation in both stocks and futures as early as November 2011, and that this behavior is common and detectable. The appropriate response is for regulators to impose frequent fines and guidance to ensure a fair market place.