Update: Author of Barron's article and Michael Lewis respond.

The February 28, 2015 weekend edition of Barron's carried an article by Bill Alpert about how trading has never been better for "The Little Guy". Alpert claimed to have arrived at this conclusion after months of studying SEC 605 reports. He further went on to rank the "Stock Wholesalers" (folks that actually execute most retail orders) and proclaimed Citadel the winner. Themis Trading wrote a must-read review of this article, so we'll avoid repeating some of the excellent points they make.

The article was filled with contempt for Michael Lewis and his book Flash Boys. Those who found themselves on the exposed side of Flash Boys last year were quick to proclaim the Barron's article to be the true story:

Many industry experts greeted the contents of Barron's article with public glee:

Even after being presented with the evidence on this page, one of these "experts" simply refuses to accept the evidence and resorts to attacking it:

What really caught our eye about the article: journalists are taking an active interest in working with market data! This is a positive development which we encourage wholeheartedly. Lobbyists and other influential companies, such as billionaire Ken Griffin's Citadel, are able to drive their agenda and policy changes through influential media, that up until now, haven't had the ability to actually look at market data and fact-check what they were being told to write.

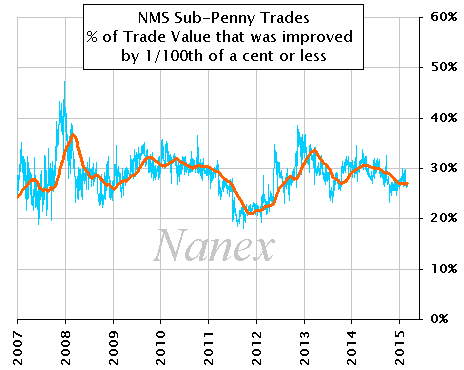

On the subject of fact-checking, Barron's suggestion that price improvement was improving went undetected by one of the many statistics we regularly track: namely, the percentage of sub-penny trades which indicate price improvement by the minimum permissible amount of 1/100th of a penny per share. Our data on this statistic is charted below. Rather than the expected drop in this value, it remains in a narrow range, indicating that over 25% of all price improved stock trades are only being improved by 1/100th of a cent per share.

This brings up a glaring omission about price improvement that the Barron's article doesn't even mention. There is a distinct loser in price improvement: the trader or investor that posts a displayed limit order to the market. Price improvement ends up costing these investors at least $1 billion a year: we have thoroughly documented this here, and discussed again here, and here, and here (you get the idea).

Back to what was included in Barron's article.

It is possible that our sub-penny indicator missed detecting a shift in price improvement. Since we had over a year of Citadel's 605 reports, we began analyzing these same reports that Barron's used for their article.

SEC 605 reports are filed monthly by participants who execute stock orders. These reports contain information about the stock orders executed by the filing firm for each stock. You can read about the fields required in these reports on the SEC's website here. Note, that only "covered orders" are in the report (details here). This is important, because order types/sizes not covered in this report are fair game to Wall Street - caveat emptor.

For each stock, orders are broken down by 5 order types:

Each order type is further broken down by order size

Barron's arranged these 4 size groups together, which makes sense because orders for 100 to 9,999 shares are covered by regulations meant to protect the retail investor.

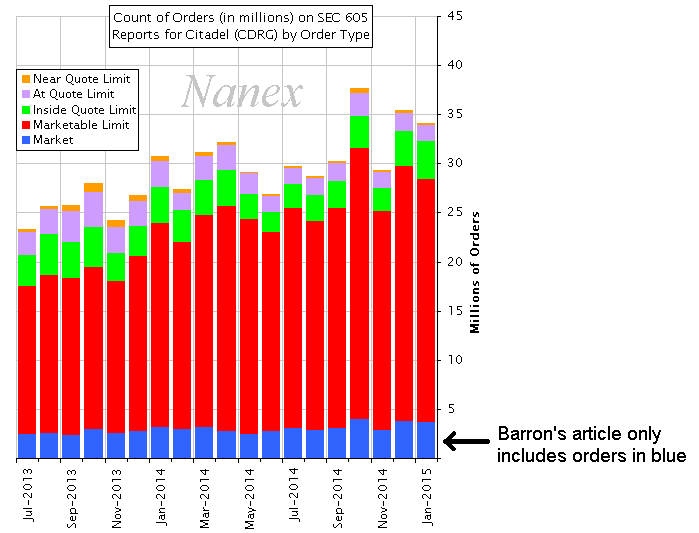

Here is a chart showing total order counts for all order sizes from Citadel, grouped into one of the 5 order types:

The first two categories, Market (blue) and Marketable Limit (red) are very similar. Marketable Limit orders are Market orders with a limit, priced to execute immediately: a buy order with a limit price higher than the current best offer, or a sell order with a limit price lower than the best bid.

After the flash crash, there was much talk in the industry about banning Market orders or converting them into Marketable Limit orders to protect retailer investors from getting executed at ridiculous "stub quote" prices (some sell orders traded at a penny and buy orders for more than $100,000). You can see from the chart that the largest order type of all is the Marketable Limit (red) and it's growing. At least at Citadel.

Therefore, if one is going to study SEC 605 reports to determine if retail investors are getting better pricing, at the very least, they would include Market and Marketable Limit orders. So upon trying to reproduce Barron's results, we used these two groups.

Our first set of results showed much lower price improvement amounts than Barron's. Re-reading the article, we found a reference indicating Citadel average $0.0048 improvement per share across the 7.6 billion shares it traded. The number 7.6 billion was less than half of the shares we counted. We realized the extras shares we were counting were all coming from the Marketable Limit orders category. After removing Marketable Limit orders from our results, our numbers matched Barron's results exactly.

Which means, Barron's was only using Market orders in their analysis.

Barron's study only includes Market orders (shown in blue above). The 4 other groups, including the biggest group - Marketable Limit orders - were discarded.

To find out why, and to make it easier for the average reader to follow, we focused on just one stock: one of retail investor's favorites: Apple Computer Corp (symbol AAPL, market cap: $753 Billion).

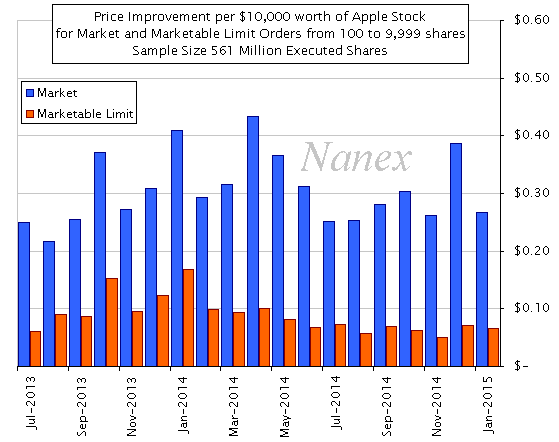

First we computed the price improvement amount, using the same Barron's formula, for each month's worth of Citadel order data for Apple stock. We separated the results for Market orders from Marketable Limits, not expecting to see much difference. We were wrong. Market orders show significantly greater price improvement than Marketable Limit orders, about 4 times more!

The image below shows the amount of price improvement for the Market orders (blue) used in Barron's study, as well as the Marketable Limit orders (orange) Barron's did not include. Market orders averaged 31 cents per $10,000 worth of Apple stock, while Marketable Limit orders averaged just 9 cents. This means for every $10,000 worth of Apple stock, the wholesaler was giving an average price improvement of 31 cents for Market orders, and just 9 cents for Marketable Limits.

If Barron's had included Marketable Limit orders in their article, readers would have seen a completely different result, as is shown clearly in the chart above. This difference becomes even more pronounced because there are many more Marketable Limit orders than Market Orders; the result would skew towards the much less impressive price improvement amounts for Marketable Limit orders (orange bars).

Barron's and their readers need to know that only about 10% of all orders from SEC 605 reports were being used in the study, and the group of orders chosen just happened to show Wholesalers in the best possible light.

The Barron's article makes no mention that it focused on the tiniest fraction of data which happens to support Wholesalers.

When searching for contact information, we came upon a the following set of comments buried in the code that Barron's published as part of the story:

This comment indicates they knew full well that Marketable Limit orders would have completely changed their story.

Normally this is where we would write a blistering conclusion. However, for a publication that commands the respect of Barron's, we've been robbed of words.

Nanex Research

Inquiries: pr@nanex.net