Nanex ~ 20-Sep-2013 ~ Einstein and The Great Fed Robbery

May 13, 2014

Business week reports ("Trading Patterns Point to Leaks Ahead of Federal Reserve

Announcements") on a research paper that found “robust evidence” that

some traders have been getting early news of U.S. Federal Reserve rate announcements

and then trading on it during the Fed’s media lockup.

We revisit the controversial release of FOMC news on September 18th 2013 using the

time stamps generated by the exchanges and included in their raw feed.

Our analysis

is consistent with a simultaneous release of the information at the CME and at the

Nasdaq colocation centres exactly at 2:00:00 pm.

It should be noted that McKay Brothers, LLC, is a leading provider of specialty

microwave telecom services between financial datacenters such as Chicago and New York and should

be considered an expert on this topic. A few quotes from

the paper:

We can safely conclude that the handover of

the FOMC announcement

did not occur in DC, it was not a lockup release.

The data is not consistent with a release in the lockup facility in Washington DC, even

at a time slightly before 2:00 pm.

Our conclusion is that the most likely scenario is that the

FOMC data was released under embargo

at 2:00 pm exactly both at Aurora and at Carteret.

Note: The High Frequency Trading Firm Virtu's attempt to discredit our findings severely backfired after closer inspection of their numbers revealed bizarre logic and bad science.

In

fact, Virtu's own data agrees with our conclusion. Read, and decide for yourself.

One of Einstein's great contributions to mankind was the theory of relativity, which

is based on the fact that there is a real limit on the speed of light. Information doesn't

travel instantly, it is limited by the speed of light, which in a perfect setting is

186 miles (300km) per millisecond.

This has been proven in countless scientific experiments

over nearly a century of time. Light, or anything else, has never been found to go faster

than 186 miles per millisecond. It is simply impossible to transmit information faster.

Too bad the bad guys on Wall Street who pulled off The Great Fed Robbery didn't pay attention in science class.

Because hard evidence, along with the speed of light, proves that someone got the Fed

announcement news before everyone else. There

is simply no way for Wall Street to squirm its way out of this one.

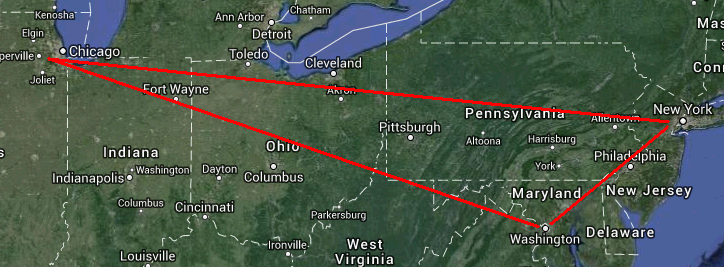

Before 2pm, the Fed news was given to a group of reporters under embargo - which means

in a secured lock-up room. This is done so reporters have time to write their stories

and publish when the Fed releases its statement at 2pm. The lock-up room is in

Washington DC. Stocks are traded in New York (New Jersey really), and many financial

futures are traded in Chicago. The distances between these 3 cities and the speed of

light is key to proving the theft of public information (early, tradeable access to

Fed news).

We've learned that the speed of light (information), takes 1 millisecond to travel 186

miles (300km). Therefore, the amount of time it takes to transmit information between

two points is limited by distance and how fast computers can encode and decode the

information on both sides. Our experienceanalyzing the impact of

hundreds of

newsevents

at the millisecond level

tells us that it takes at least 5 milliseconds

for information to travel between Chicago and New York. Even though Chicago is

closer to Washington DC than New York, the path between the two cities is not straight

or optimized: so it takes information a bit longer, about 7 milliseconds, to travel

between Chicago

and Washington. It takes little under 2 milliseconds between Washington and

New York.

Therefore, when the information was officially released in Washington, New York should

see it 2 milliseconds later,

and Chicago should see it 7 milliseconds later. Which means we should see a reaction in stocks (which trade in New York) about 5 milliseconds before

a reaction in financial futures (which trade in Chicago). And this is in fact what we normally see

when news is released from Washington.

However, upon close analysis of millisecond time-stamps of trades in stocks and futures

(and options, and futures options, and anything else publicly traded), we find that

activity in these instruments exploded in the same millisecond. This is a physical

impossibility. Also, the reaction was within 1 millisecond, meaning

it couldn't have reached Chicago (or New York): another physical impossibility. Then there is the case that information

on the Fed Website was not readily understandable for a machine

- less than a thousandth of a second is not enough time for someone to commit well

over a billion dollars that effectively bought all stocks, futures and options.

The Data

Fortunately for us, in the minutes before the Fed announcement at 14:00 on September 18, 2013, there was significant

activity in Comex Gold Futures (traded in Chicago) and the ETF symbol GLD (traded in

New York). This gives us an opportunity to measure closely, the exact (to the millisecond)

amount of time between trading activity in Chicago and

New York. The first chart shows

about 3.5 minutes of time around the Fed Announcement release, giving us an overview. The

stack of charts that follow allow you to easily compare between GLD (New York) and

GC Futures (Chicago) for

6 different active periods. You will see that in the first 5 pairs - before the announcement,

activity first shows up in GC Futures, followed by activity in GLD between 5 and 7 milliseconds

later. In the last pair, which compares activity at exactly 2pm (14:00:00), you will see both

GC futures and GLD react in the same millisecond of time.

1. Animation of December 2013 Gold (GC) Futures (Chicago) followed by GLD stock (New York) on September 18, 2013 from 13:57 to 14:00:30.

2. Zooming in 150 milliseconds of time for 6 different high activity periods minutes

before and during the annoucement.

Each chart shows first, Gold Futures (GC - traded in Chicago) followed by GLD (traded in New York). The first 5 charts show events minutes before the news release: you can clearly see that Gold Futures (GC) trades before GLD.

But the last chart shows the event at 14:00:00, where Gold Futures trades at the exact same time as GLD stock. This is physically impossible unless information

was already present in Chicago and New York. It's easiest if you compare the bottom

panels of each chart which shows trading volume for each millisecond.

The charts below show that stocks in New York react about 5 milliseconds before futures

in Chicago. All examples on this page use the same source of time stamps: from the exchanges.

Which means anyone will be able to reproduce these

charts from exchange data.

Conclusion

There are 2 possibilities, and both aren't good news for Wall Street.

1. A Timed News Release by a News Organization

The Fed news was condensed by a news service into a simple "No Tapering" message (something easily readable by a machine) and then placed on news servers co-located next to trading machines in both New

York and Chicago at some time before 2pm. The news machines are programmed to release

the information at precisely 2pm, allowing

the algos to react immediately at both locations. This is how some news services release

privately compiled statistics like the Consumer Confidence or Chicago PMI. In those cases, we see

the exact behavior as in the last chart above - an immediate reaction in New York and Chicago. But the Fed news was released from a lock-up room which prevents transmission

of any information to the outside world. Also, if it was a timed news release, the data

was released before 2pm relative to Washington (when it's 2pm in Chicago, it's

actually 1:59:59.995 relative to Washington). Given that several large news organizations

were recently caught clandestinely

sending news early

we think it's less likely they would do something so bold, so soon.

2. Leaked to Wall Street

The Fed news was leaked to, or known by, a large Wall Street Firm who made the decision

to pre-program their trading machines in both New York and Chicago and wait until

precisely 2pm when they would buy everything available. It is somewhat fascinating that

they tried to be "honest" by waiting until 2pm, but not a thousandth of a second

longer. What makes this a more likely explanation is this:

we've found that news organizations providing timed

release services aren't so good about synchronizing their master clock - and often release

plus or minus 15 milliseconds from actual time. Their news machines in New

York and Chicago still release the data at the exact same millisecond, but with

the same drift in time as the master clock. That is, we'll see an immediate market

reaction at say, 15 milliseconds

before the official scheduled time, but in the same millisecond

of time in both New York and Chicago. Historically, these news services have shown

a time range of about 30 milliseconds (+/- 15ms), and since this event started within

1 millisecond, it means the odds favor a leak over a timed news service.

What also makes this the more likely conclusion is this: we know the Bureau of Labor

Statistics has recently hardened access to their lock-up room, weeding out all but respected

news organizations. So imagine a reporter for one of these news organizations who is

tasked with

distilling the Fed news into a simple message that machines could read in less than

a millisecond and interpret to mean, "buy all the things now". It's unlikely that

Wall Street would place so much responsibility on one news reporter. Unless that

reporter was a skilled - perhaps, dare we say, incentivized - trader. We think it's

unlikely that a respected news organization would tolerate this clandestine behavior.

Too much like crooks sneaking around at night.

Regardless of which possibility is correct (it could even be a combination of the two),

the Fed news was certainly present in trading centers in Chicago and New York before

2pm. The evidence is overwhelming. It is unknown how many people had access to this

information - for a timed news release, it would have been at least an administrator,

probably Q.A. and others. What we do know is the resulting explosion of trading just

1 thousandth of a second after 2pm, was unprecedented in the history of Fed news announcements,

and much of that trading was based on information obtained before the set Federal Reserve

Board release time.

Update: September 25, 2013

A few articles covering this are focusing on trading in Gold. We singled out gold, is

because it was one of the few instruments with high activity in the minutes before the

2pm announcement. This high activity preceeding the release allowed us to verify that

the exchange time stamps we used later, were accurate.

It wasn't just gold. It was everything that traded. In fact, the 1/100th of a second

after 2pm was the most active 10 milliseconds in the history of the U.S. Stock an Futures

markets. See charts here and

here.

Update: September 26, 2013

We added charts (see below) that compare market reactions from

previous events driven by news from Washington DC. These clearly show how New York markets

respond about 5 milliseconds before Chicago.

Update: October 3, 2013

The FIA Principal Traders Group (FIA

PTG), a major lobbyist group for High Frequency Traders (HFT), has come out with a statement along with this

Financial Times article that corroborates our findings: that the Federal Reserve

FOMC "no taper" information was in Chicago and New York before it was released at 2pm

in Washington, D.C. Reading between the lines, it appears the leak was from one or more

news services which secretly uploaded this valuable news to computers in Chicago and

New York minutes before 2pm. This scenario is possibility #1 that we wrote in our conclusion below. The FIA PTG also confirms that Virtu's

(a major HFT that attempted to discredit this paper) analysis was wrong, which we debunked here.

Update: October 28, 2013

The Fed will install an Internet Kill Switch for future releases. More

here.