Nanex Research

Nanex ~ 28-Sep-2013 ~ Shredding Virtu's Response with

Science

Note: Chris Concannon, a partner at Virtu, didn't respond to 5 phone calls and emails

seeking comment on this paper,

according to Bloomberg.

The High Frequency Trading (HFT) firm Virtu published a response to our analysis, Einstein and The Great Fed Robbery,

in which we showed that Fed FOMC news had to exist in New York and Chicago before it was released at 2pm in Washington D.C.

Although it may appear to some that Virtu’s intent was to discredit our work, we will show that Virtu's own data actually corroborates our findings: Virtu's paper, in fact, agrees with our analysis.

Direct quotes from Virtu’s paper in italics.

- Virtu states that their timestamps are accurate and synchronized between NY and Chicago.

..our clocks in New York and Chicago are synchronized automatically to the same GPS antenna which ensures that the two clocks are synchronized to each other.

- Virtu’s timestamp of SPY's first trade in New York is 0.397 milliseconds

after

2pm.

Relying on our two sources of market data timestamps, our records show that the first trade immediately following the Fed release at 2 PM in SPY occurred at 2:00:00.000397

- Virtu’s timestamp of Gold Futures first trade in Chicago is 2.034 milliseconds

after 2pm.

The first trade for the December 2013 Gold Future contract on CME was recorded by our system at 2:00:00.002034.

- Virtu calculates that news from Washington arrives in Chicago at least 2.1

milliseconds after New York. It would be physically impossible for a reaction in Chicago to occur less than 2.1 milliseconds after New York.

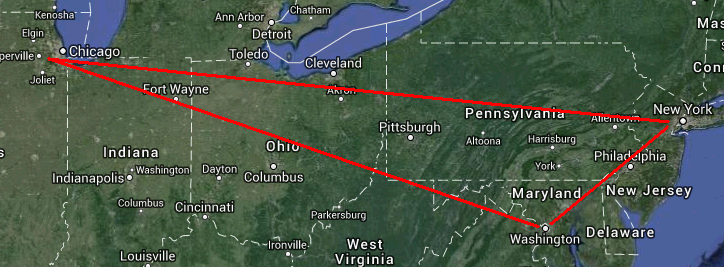

The straight line distance from Washington, D.C. to New York is approximately 204 miles. The straight line distance from Washington, D.C. to Chicago is approximately 595 miles. Any signal leaving Washington, D.C. will arrive in Chicago at least 2.1 milliseconds after arriving in New York since that is the time it takes light to travel the additional 391 miles to Chicago.

All we have to do is show that trading begins in Chicago less than 2.1 milliseconds after trading begins in New York. We’ll use Virtu’s timestamps from (2) and (3) above. Times are milliseconds after 2pm.

2.034 market reacts in Chicago

-0.397 market reacts in New York

1.637 milliseconds that Chicago trades after New York.

Thus, Virtu’s accurate, synchronized timestamped data shows that trading begins in Chicago 1.637 milliseconds after trading begins in New York.

1.6 is not greater than 2.1 - unless this is some kind of new math.

Maybe there is some kind of new math going on, as here is Virtu’s accounting for the reaction time difference:

The timestamp values almost line up perfectly with the minimal 2.1 millisecond figure for the difference in travel time between DC to Chicago and DC to NY

The value 1.637 does not almost line up perfectly with the minimal

2.1 millisecond figure. When dealing with the absolute limit of the speed of light, even 1 trillionth of a second faster would violate our physical understanding of the world. If the difference was 2.099999 instead of 1.637 it would still be suspect.

There is more

Virtu’s calculations rely on the speed of light being 186.2 miles per millisecond (391 miles in 2.1 milliseconds from their paper), which is pretty close to how fast light travels under ideal conditions (a vacuum such as in space). But reality is far from perfect. For example, the earth is curved, there are mountains and other obstacles such as cities, CIA restricted areas, Naval airspace, and private land, just to mention a few. Then of course, one has to get the signal from inside the Fed lock-up room to the outside world: something we are pretty sure is under the control of the Federal Government, an entity that is probably a lot more concerned about security (firewalls) than speed.

Bottom line: it's a lot more complicated than simply using straight line distance and ignoring the realities of our world. But even if we use the ideal case we can still prove that Fed news was released to high frequency trading firms early.

In the ideal case, for Chicago to react 2.034 ms after 2pm, information had to leave Washington at least 1.16 milliseconds before 2pm. In the real world, that number will be much higher. Our analysis

of market reaction times for other news releases from Washington shows it takes about 7 milliseconds before Chicago reacts.

And finally, Virtu admits that the Fed news had to leave Washington before 2pm - (not enough wiggle room in the numbers, perhaps):

In fact, the data seems to indicate that the signal left Washington, D.C some time before 2 PM. But it clearly shows that the trading in New York and Chicago is consistent with both locations receiving the same signal originating from Washington, D.C.

The second sentence we’ve already proven to be false, unless of course 1.637 is greater than 2.1. But that first sentence needs some explaining.

Virtu uses microsecond timestamps throughout their paper. Microseconds are millionths of a second. Virtu emphasizes the importance of precision, and yet, when it comes to the actual question of whether or not the Fed news was leaked (released before “precisely 2pm” as the Federal Reserve has stated), Virtu simply writes that the Fed news was released

“some time before 2pm”. Is that a new S.I. unit of time? What is the conversion factor between “some time” and microseconds?

Conclusion

Virtu’s own data shows that Fed news had to exist in New York and Chicago “some time”

before it was released at 2pm in Washington D.C.

Coming up next: Using data and comments from the same Virtu paper, we will prove that direct feeds give high frequency traders an illegal speed advantage. We believe this is a matter more serious than the leak of Fed news. Now Published.

Nanex Research

Inquiries: pr@nanex.net