On September 14, 2012, the financial story of the day was a press release from the SEC

titled: SEC Charges New York Stock

Exchange for Improper Distribution of Market Data. We were

stunned, because for two years, we have published an abundance of incontrovertible

evidence of consolidated data feed delays, starting with the NYSE delay that contributed to, if not caused,

the flash crash on May 6, 2010 (we even built a tool allowing others to replicate the results). When

we presented evidence of the NYSE delay, it was vigorously denied. Even the SEC was

skeptical at a July 8, 2010 presentation we gave at the CFTC offices in Washington.

The following month we published a paper showing how delays in the consolidated feed

could be created at will. Finally, on August

24, 2010, the NYSE admitted to the May 6, 2010 delay and claimed the

problem was corrected. Though our study of GE on July 21, 2010 was based on data after they

claimed it was fixed.

But what is even more stunning about the SEC press release is the confirmation of the

importance

of the consolidated data feed. From the first paragraph of the SEC order against the NYSE:

When Congress mandated a national market system (“NMS”) for trading securities

in 1975, it emphasized that consolidated data “would form the heart of the national

market system.” The Commission since has emphasized the importance of the consolidated

data feeds on many occasions, including in its January 2010 Market Structure Concept

Release: “As a result, the public has ready access to a comprehensive, accurate, and

reliable source of information for the prices and volume of any NMS stock at any time

during the trading day. This information serves an essential linkage function by helping

assure that the public is aware of the best displayed prices for a stock, no matter

where they may arise in the national market system.” In addition to providing the

view of the market for many investors, consolidated data feeds also play an important

role in price discovery and compliance functions. For example,

a number of exchanges

and other trading centers use the consolidated feeds to check prices at other trading

centers to determine whether they may execute an order or whether another trading center

has a better price.

In the many examples we have come across showing delayed data in the consolidated feed,

the NYSE rarely shows up as one of the exchanges involved. Therefore we expect to see

similar actions taken against other exchanges in the coming weeks.

The disparities in data transmissions that Rule 603(a) prohibits can have

important consequences that risk undermining investor confidence and interfering with

the efficiency of the markets. For example, a delay in the release of data to the consolidated

feeds in contrast to the proprietary feeds can cause an investor relying on the consolidated

feeds to make a trading decision based on a potentially stale picture of current market

conditions. An exchange’s delay in sending its quotes to the consolidated feeds also

can cause inefficient execution decisions at other market centers and, under some circumstances,

create the appearance of a “crossed” national best bid and offer (“NBBO”), which occurs

when the best bid exceeds the best offer. The

appearance of a crossed NBBO can cause both uncertainty and the risk of a trade

being executed at worse than the best available price. 6

6 A crossed NBBO triggers an exception to the trade-through rule of Regulation

NMS. See Rule 611(b)(4) of Regulation NMS, 17 CFR § 242.611(b)(4).

From Regulation NMS

Rule 611(b)(4) Exceptions to Order protection rule:

(4) The transaction that constituted the trade-through was executed at a

time when a protected bid was priced higher than a protected offer in the NMS stock.

What this means is that when the NBBO is crossed (the best bid price is higher than

the best offer price), exchanges do not have to route orders and are free to execute

trades locally, regardless if better prices exist elsewhere. How often is the NBBO crossed?

It depends greatly on market activity. During news announcements, there can be 500

to 1,000 or more crossed NBBO quotes. The lowest number of crossed quotes ever seen

in a minute (during quiet trading) is about 25.

Crossed NBBO quotes may be one cause of the dozens of micro

flash-crashes we see in stocks every day. If a large orders appears

while a stock has a crossed quote, the order could execute against the local book (depriving

it of liquidity on other exchanges) leading to a sudden price drop (or rise). It is

both curious and incongruous that the SEC then goes out of their way to write on page

7:

Although the data delays came to light during the inquiry regarding the

Flash Crash, the delays occurred after the start of the Flash Crash and did not cause

the extreme volatility that day.

We strongly disagree and would like to see what evidence (if any) they have to make

such a bold claim.

The Consolidation Delay Myth

The SEC Order persists a myth that the consolidation process adds approximately 5-10

milliseconds of delay:

The Commission has recognized that, due to the consolidation process (i.e.,

the time from the receipt by the Network Processor of the information from exchanges

to the time it distributes consolidated information to the public), information from

a Network Processor generally reaches market participants later than information from

exchanges’ proprietary feeds. See Concept Release, 75 Fed. Reg. at 3601 (citing an average

consolidation time of approximately 5-10 milliseconds). Nevertheless, exchanges have

an obligation under Rule 603(a) to take reasonable steps to ensure—through system architecture,

monitoring, or otherwise—that they release data relating to current best-priced quotations

and trades through proprietary feeds no sooner than they release data to the Network

Processor, including during periods of heavy trading.

To dispel this myth, we spent considerable time and effort creating an animation tool that illustrates how all market participants (even one subscribing to direct

feeds only)

would have to replicate this consolidation process.

This video shows 11 exchanges

trading one stock. The box at 6 o'clock represents the network processor or SIP. The

other boxes each represent one exchange trading this stock. The lines connecting

the boxes represent direct feed connections. As you can see, any entity connected

to each exchange must essentially replicate the consolidation

process performed by the SIP.

The SIP shows the National Best Bid/Offer. Watch how much it changes in a fraction of a second.

The shapes represent quote changes which are the result of a change to the top of the

book at each exchange. The time at the top of the screen is the time of the last quote

or trade update in Eastern Time HH:MM:SS:mmm (mmm = millisecond). We slow time down

so you can see what goes on at the millisecond level. A millisecond (ms) is 1/1000th

of a second. The blink of an eye is about 200 ms. Note how every exchange must process

every quote from the others -- for proper trade through price protection. This complex

web of technology must run flawlessly every millisecond of the trading day, or arbitrage

(HFT profit) opportunities will appear. It is easy for HFTs to cause delays in one or

more of the connections between each exchange.

The Next Steps

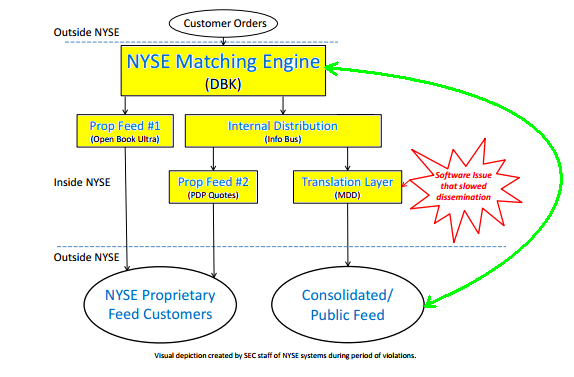

The SEC press release provided a visual depiction of NYSE's system and showed where the delay occurred.

This is a good start. The next step is filling in the details. Such

as what happens to orders when they enter the "NYSE Matching Engine"

and how these

orders might be routed to other exchanges based on prices from the "Consolidated/Public

Feed". We added the green line linking these two systems below:

We can infer from the SEC Order that the two systems pointed to by the green arrow must

somehow be connected.

From page 4 of the SEC Order:

NYSE receives hundreds of millions of orders to buy or sell securities each

trading day. These orders and related message traffic go to NYSE’s matching engine,

known as the Display Book, or “DBK,” for processing. DBK matches orders and generates

executions, redirects orders for routing to other exchanges, and maintains limit orders

in NYSE’s “order book” for possible future execution.

and from paragraph 1 of the same order:

..a number of exchanges and other

trading centers use the consolidated feeds to check prices at other trading centers

to determine whether they may execute an order or whether another trading center

has a better price.

In other words, the SEC has stated that exchanges must use the consolidated feed to

check prices when determining order routing, and we know from the SEC diagram that the

"DBK" system at the NYSE is what redirects orders for routing to other exchanges.

But we highly doubt this is how routing actually works.

The other items to note from the SEC diagram:

Why is "Prop Feed #1" connected to "DBK" and not "Internal Distribution" ?

Are there any other connections to the yellow boxes which are "Inside NYSE" that lead to systems

that could act on that information?

What incentive does the NYSE (or any exchange) have to upgrade computers and networks

serving the Consolidated Feed first?

Any computer (box) has the potential to cause sub-second delays that remain hidden

when averaging latencies at 1 second or higher intervals.

Eventually, on every public exchange, the SEC needs to document every system and network

that an order flows through, from the time the order is created until

the time it is either

cancelled or executed and reported on both the private and public datafeeds. For orders

that are executed and become trades, the SEC needs

to document every system and network that the trade flows through, until it is reported

on both the private and the public datafeeds.

We predict there will be several surprises, some that will make NYSE's violation

pale by comparison.